42011 Date of Issue. Restriction On Deductibility Of Interest under Section 140C of the Income Tax Act 1967 and Income Tax Restriction On Deductibility Of Interest Rules 2019 PU.

Overview Of Malaysian Taxation By Associate Professor Dr Gholamreza Zandi Ppt Download

INLAND REVENUE BOARD MALAYSIA INCOME FROM LETTING OF REAL PROPERTY Public Ruling No.

. B Page 1 of 26 1. Section 4f of the Income Tax Act 1967 the Act which is derived from Malaysia and received by a nonresident is - subject to WT of 10 under Section 109F of the Act. Charge of income tax 3 A.

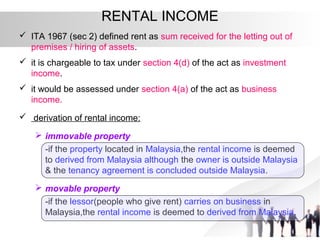

A Page 1 of 13. Rental income is generally assessed under Section 4 d Rental Income of the Income Tax Act and is seen as income from investment. Income Tax Act Part.

Payments that are made to NR payee in respect of the above income are subject. The determination of whether a payment made to a non-resident falls under Section 4f depends on the facts and circumstances of each case. All the units are let out to several tenants.

Notwithstanding section 4 and subject to this Act the income of a person not resident in Malaysia for the basis year for a year of assessment in respect. 4 Laws of Malaysia ACT 53 Section 11. This R uling explains.

Chapter 4 - Adjusted income and adjusted loss Section. The prevailing WHT rate is 10 except where a lower rate is provided in an applicable tax treaty. Any particular dealing or transactions must come within the walls of scope.

Resident individuals are taxed according to the tax rate and eligible for tax reliefs in accordance with section 45A - section 49 of the ITA 1967. INCOME FROM LETTING OF REAL PROPERTY INLAND REVENUE BOARD Public Ruling No. Section 4 2 of Income Tax Act.

In respect of income chargeable under sub-section 1 income-tax shall be deducted at the source or paid in advance where it is so deductible or payable under any provision of this Act. It will also give the readers an overview of what is income in revenue law. The DGIR is time-barred under section 911 of the Income Tax Act 1967 from raising the Notice of Assessment for the YA 2010.

Section 138A of the Income Tax Act 1967 ITA provides that the Director General of. The new guidelines are broadly similar to the earlier guidelines and explain the penalties that will be imposed under Section 1123 of the Income Tax Act 1967 ITA Section 513 of the Petroleum Income Tax Act 1967 PITA and Section 293 of the Real Property Gains Tax Act 1976 RPGTA where a taxpayer fails to furnish a tax return within. Income under Section 4f ITA 1967.

Income that a non-resident derives from Malaysia from special classes of income is subject to tax in Malaysia. A Public Ruling as provided for under section 138A of the Income Tax Act 1967 is issued for the purpose of providing guidance for the public and officers of the Inland. 11 the treatment of rent as a non-business source of income under section 4d of the Income Tax Act 1967 the Act.

And often allow notional reductions of income. In Malaysia income tax is generally governed by Income Tax Act 1967 Act 531967. Clue of what section 4 Income Tax Act 1967 trying to classify.

If the premise is a special purpose commercial building like a factory warehouse. 1 In ascertaining the adjusted income of a person. Throughout Malaysia--28 September 1967 PART I PRELIMINARY Short title and commencement 1.

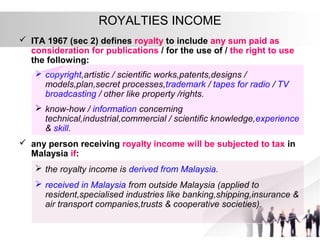

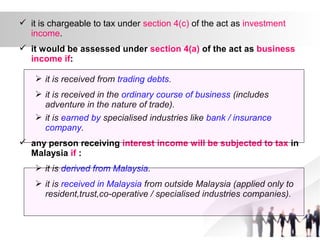

Income falling under Section 4f of the Income Tax Act 1967 ITA 1967 includes any other income that is not obtained from business employment dividends interests discounts rents royalties premiums pensions or annuities. The date of commencement of renting is on the first. A company can have its rental income assessed as Section 4 a business income if it is letting at least 4 units of commercial buildings 4 floors of shop houses 4 units of residential properties or any combinations of 4 units of the type of premises mentioned.

The Respondent incorrectly imposed a penalty under Section 1132 of the ITA at the rate of 45. 1341 Sales Tax 13411 Effective date and scope of taxation Sales tax is a single-stage tax imposed on taxable goods manufactured locally by a registered manufacturer and on taxable goods imported by any person. 19 December 2018 Example 2 Wahida owns a 4-storey building consisting of 32 units that can be used as offices and shop lots.

Income falling under paragraph 4 f chargeable to tax 41 The introduction of a new section 109F of the ITA with effect from 01012009 provides a mechanism to collect withholding tax from a non-resident person who receives income which is derived from Malaysia in respect of gains or profits that fall under paragraph 4 f of the ITA. The Income Tax Act 1967 which is referred to as the principal Act in this Chapter is amended in subsection 51a by inserting after the words 109d the words 109da in respect of a non-resident unit holder other than an individual. As a guidance the criteria.

INLAND REVENUE BOARD OF MALAYSIA Date of Publication. The gains from the disposal of properties are not subject to section 4a of the ITA. Translation from the original Bahasa Malaysia text Issue.

Paragraph 4a amended by Act 578 of 1998 s9a by. PART III - ASCERTAINMENT OF CHARGEABLE INCOME Chapter. An Act for the imposition of income tax.

10 March 2011 Issue. While non-resident individuals are taxed at a flat rate of 30 and are not eligible to enjoy any reliefs. INCOME TAX ACT 1967 Incorporating all amendments up to 1 January 2006 053e FM Page 1 Thursday April 6 2006 1207 PM.

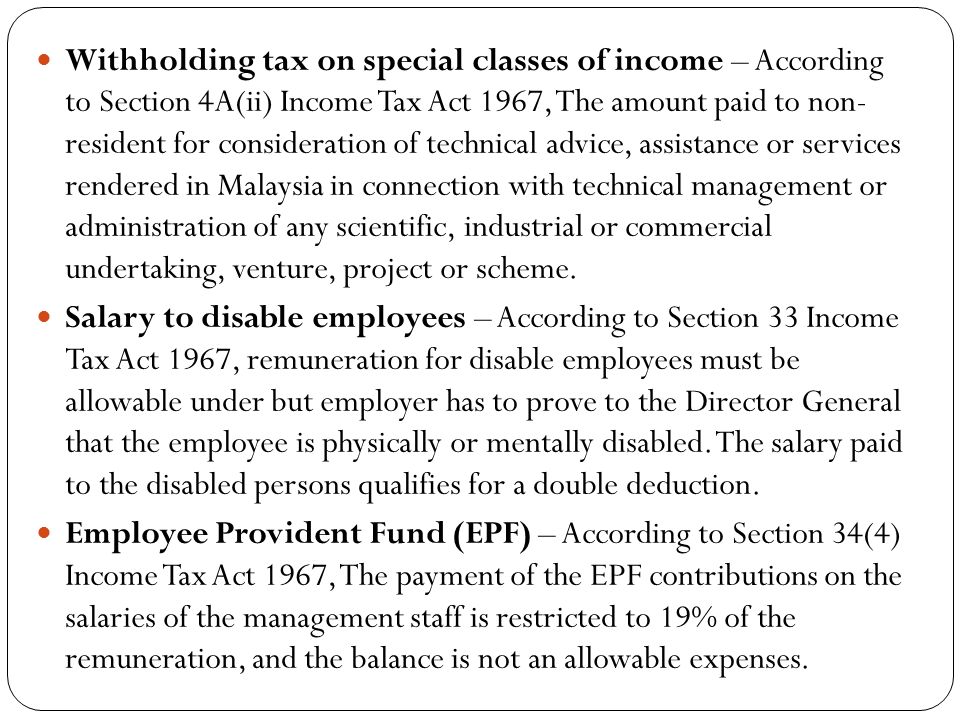

When rental income is assessed under section 4 d it has to be grouped into three sources namely residential properties commercial properties and vacant land. Special provisions applicable to adjusted income from a business. The special classes of income are those listed in Section 4A of the Income Tax Act 1967 ITA.

134 Indirect taxes Sales Tax and Service Tax SST came into effect in Malaysia on 1 September 2018. Non-chargeability to tax in respect of offshore business activity 3 C. Under Section 304 Income Tax Act 1967 where a taxpayer had previously claimed a tax deduction or capital allowance and the amount of debt is then released it would be treated as being part of the debtors gross income and hence taxable in the Year of Assessment in which the debt was forgiven.

Short title and commencement 2. And there are parts which have been customised to ensure adherence to the Act and Inland Revenue Board of Malaysias IRBM procedures as well as domestic circumstances. Interpretation PART II IMPOSITION AND GENERAL CHARACTERISTICS OF THE TAX 3.

30 Jun 2004. Finance 9 Amendment of section 5 4. 1 This Act may be cited as the Income Tax Act 1967.

Derivation of business income in certain cases 13. 12004 MALAYSIA Date of Issue. LAWS OF MALAYSIA Act 53 INCOME TAX ACT 1967 ARRANGEMENT OF SECTIONS PART I PRELIMINARY Section 1.

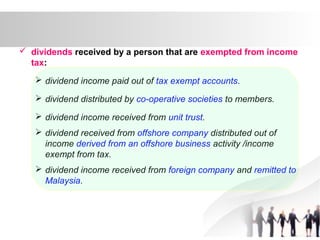

Any source of income derived from outside Malaysia and received in Malaysia is tax exempted.

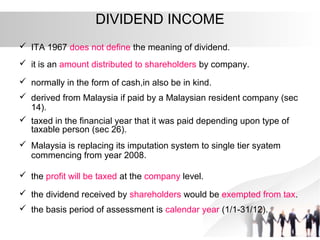

Taxation Principles Dividend Interest Rental Royalty And Other So

Taxation Principles Dividend Interest Rental Royalty And Other So

Problem Based Learning Project Tax Computation On Malaysian Food Service Mfs Sdn Bhd Group B Namematrik No Izwani Bt Abdul Majid Hazwani Bt Ghazali Ppt Download

What Is Local Income Tax Types States With Local Income Tax More

Tax Exemptions Deductions And Credits Explained Taxact Blog

Taxation Principles Dividend Interest Rental Royalty And Other So

2

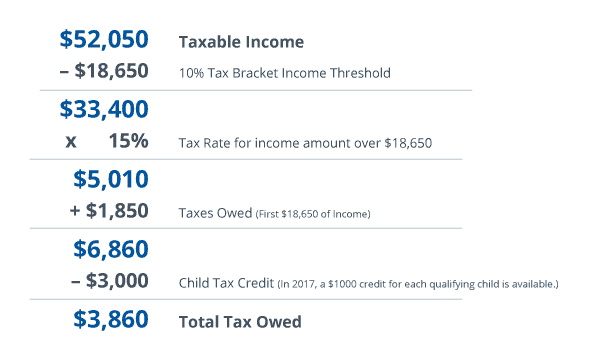

Taxable Income Formula Examples How To Calculate Taxable Income

Flowchart Final Income Tax Download Scientific Diagram

Problem Based Learning Project Tax Computation On Malaysian Food Service Mfs Sdn Bhd Group B Namematrik No Izwani Bt Abdul Majid Hazwani Bt Ghazali Ppt Download

Taxation Principles Dividend Interest Rental Royalty And Other So

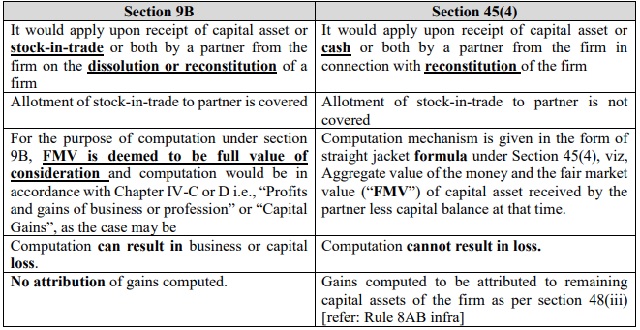

Redesigned Taxation On Reconstitution Dissolution Of The Firm A New Jeopardy Capital Gains Tax India

Taxation Principles Dividend Interest Rental Royalty And Other So

Irs Releases 2020 Tax Rate Tables Standard Deduction Amounts And More

2

Taxation Principles Dividend Interest Rental Royalty And Other So

Taxation Principles Dividend Interest Rental Royalty And Other So

Rental Income Tax Malaysia And Other Tax Reliefs For Ya 2021

The 4 Income Tax Systems Around The World